HONG KONG, March 30th, 2026 —— CIC extends our warmest congratulations to EpiWorld Electronic Technology (Xiamen) Co., Ltd. (02726. HK) on its successful listing on the Hong Kong Stock Exchange (HKEX) today.

CIC's Collaborative Journey to the Listing

Throughout the listing process, CIC provided end-to-end support to the company and its sponsors:

Drafted and compiled the industry overview chapter of the prospectus, laying a solid research foundation for the formal listing application.

Assisted in responding to inquiries from regulatory authorities, ensuring comprehensive and accurate disclosure.

Refined listing application materials continuously to meet stringent market and regulatory requirements.

EpiWorld – Global Leader in Silicon Carbide Epitaxial Wafers

EpiWorld is a global leader in silicon carbide epitaxial wafers. According to CIC research, the Company has been the world's largest SiC epitaxial supplier by annual sales volume since 2023, commanding a market share exceeding 30% in 2024. EpiWorld is also the first enterprise to commercialize 8-inch SiC epitaxial wafers in the open market.

The Company is primarily engaged in the research, development, production and sales of SiC epitaxial wafers. Through both epitaxial wafer sales and epitaxial wafer foundry service models, EpiWorld provides downstream customers with high-quality SiC epitaxial products and manufacturing services. Leveraging its long-accumulated epitaxial growth process capabilities and product development expertise, the Company has established a comprehensive product portfolio covering 4-inch, 6-inch and 8-inch SiC epitaxial wafers, capable of meeting diverse customer requirements across different dimensions, specifications and application scenarios.

Furthermore, the Company led the drafting and establishment of the world's first and only SiC epitaxy industry standard by SEMI (Semiconductor Equipment and Materials International) – "SEMI M092-0423 Specification for 4H-SiC Homo-epitaxial Wafer", and was the first globally to launch 12-inch SiC epitaxial wafer products.

Global Power Semiconductor and SiC Power Semiconductor Device Industry Overview

Power semiconductor devices serve as core components in electronic systems for power conversion and circuit control. Through functions including rectification, inversion, power amplification, power switching and circuit protection, these devices regulate energy flow and ensure system stability. Based on material composition, power semiconductor devices are primarily categorized into conventional silicon-based semiconductors and wide bandgap semiconductors, with the latter mainly comprising silicon carbide (SiC) and gallium nitride (GaN).

SiC power semiconductor devices demonstrate superior performance characteristics in breakdown voltage, thermal conductivity, electron saturation velocity and radiation resistance, offering broader applicability in medium-to-high voltage applications above 600V. These devices are increasingly deployed across electric vehicles (EVs), charging infrastructure, renewable energy, energy storage systems, as well as emerging applications including home appliances, AI computing and data centers, smart grids and eVTOL (electric vertical take-off and landing) aircraft.

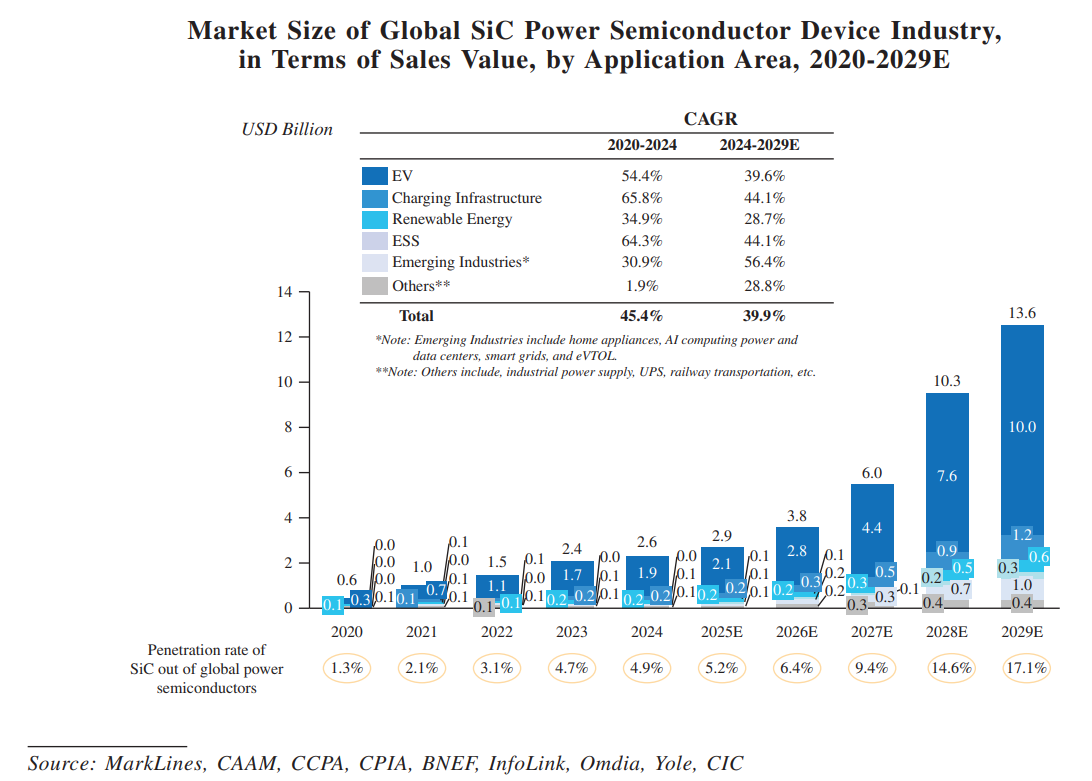

The global SiC power semiconductor device market remains in a rapid growth phase. Market size expanded from US$0.6 billion in 2020 to US$2.6 billion in 2024, representing a compound annual growth rate (CAGR) of 45.4%. The market is projected to further grow to US$13.6 billion by 2029, with a CAGR of 39.9% from 2024 to 2029. Concurrently, the penetration rate of SiC power semiconductor devices in the global power semiconductor market is expected to increase from 4.9% in 2024 to 17.1% by 2029, indicating substantial industry growth potential.

SiC epitaxial wafers serve as critical foundational materials in the manufacturing process of SiC power semiconductor devices, occupying a core position in the upstream industry chain. As single-crystal SiC thin films grown on substrate surfaces, epitaxial wafers enable precise control of doping type, concentration and thickness to meet diverse device design requirements. Given the inherent challenges in achieving precise doping control and effectively reducing crystal defects in single-crystal substrates alone, SiC device manufacturing typically requires high-quality epitaxial layers grown on substrate surfaces. Consequently, epitaxial wafers have become essential foundational materials in the SiC industry chain, with epitaxial layer quality significantly impacting end-device performance.

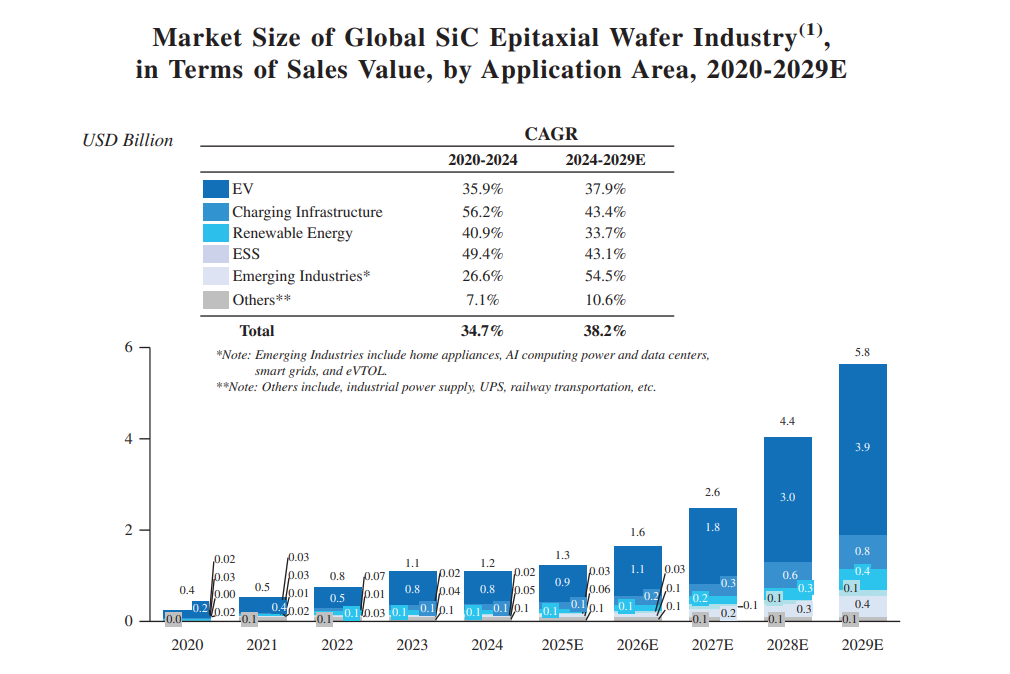

The global SiC epitaxial wafer market has experienced continuous growth in recent years, with market size increasing from US$0.4 billion in 2020 to US$1.2 billion in 2024, representing a CAGR of 34.7%. The market is projected to reach US$5.8 billion by 2029, with a CAGR of 38.2% from 2024 to 2029. Electric vehicles represent the largest application segment, with related market size expected to reach US$3.9 billion by 2029. Additionally, charging infrastructure, renewable energy, energy storage systems and emerging application areas maintain robust growth momentum, continuously driving industry expansion.

Key Driving Factors of SiC Power Semiconductor Devices and Epitaxial Wafers Market Growth(According to CIC)

1. Continued Expansion of Core Downstream Applications Drives Demand for SiC Epitaxial Wafers

Driven by the global energy transition and electrification trends, the market demand for high-performance, high-efficiency power semiconductor devices is increasing. Leveraging superior thermal performance, high breakdown voltage, low switching losses, and the ability to enhance overall system efficiency, SiC power semiconductor devices are being rapidly adopted in core sectors such as EVs, renewable energy, and energy storage systems to meet higher performance and efficiency requirements. Meanwhile, the continuous expansion of emerging application scenarios—including home appliances, AI computing, data centers, smart grids, and eVTOL—is further fueling the growth of the SiC power semiconductor device market. From 2024 to 2029, the global SiC power semiconductor device market is expected to grow at a CAGR of 39.9%. As a critical foundational material for device manufacturing, demand for SiC epitaxial wafers will rise in tandem with the expansion of the downstream device market, providing sustained growth momentum for the global SiC epitaxial industry.

2. Technological Advancements and Manufacturing Scale-Up

Innovations in epitaxial growth technology, defect reduction, and improved uniformity are enhancing the quality and yield of SiC epitaxial wafers, making them more cost-effective and reliable. The maturation of 6-inch SiC epitaxial wafer manufacturing processes, reduction in production costs, breakthroughs in the mass production of 8-inch SiC epitaxial wafers, and accelerated commercialization are driving rapid growth in the SiC epitaxial wafer market.

3. Government Policy Support

Governments worldwide are increasingly enacting favorable policies, laws, and regulations that support the development of the SiC epitaxial industry. In September 2023, the European Union enacted the European Chips Act, investing over €43 billion to advance the European semiconductor industry. The United States passed the CHIPS and Science Act in 2022, enhancing R&D and manufacturing capabilities through tax incentives and subsidies. Concurrently, the Chinese government has also introduced a series of supportive policies. In July and August 2023, the Ministry of Industry and Information Technology issued the Implementation Opinions on Improving Manufacturing Reliability and the 2023–2024 Stable Growth Action Plan for the Electronic Information Manufacturing Industry, emphasizing the need to establish industry standards and improve the reliability of wide-bandgap power semiconductor devices, including SiC power devices. In February 2023, the State Council of the People’s Republic of China issued the Outline for Building a Strong Quality Country, explicitly advocating for the development of quality, stability, and applicability of domestic materials through technological R&D. As a key material for wide-bandgap semiconductors, SiC epitaxial wafers are supported by national industrial policies and receive funding for development in critical areas.

As a seasoned Industry Consultant, CIC offers services such as market sizing, competitive analysis, and enterprise value verification, etc., with global experience in advising "first-in-sector" IPOs in the electronic technology and semiconductor sectors.

From IPO preparation to listing hearings, CIC unearths the true intrinsic value of enterprises and translates it into actionable insights for successful capital market landing. Prior to EpiWorld, CIC has supported leading enterprises in successful listings both domestically and overseas, including MiniMax, Biren Technology, Horizon Robotics and Baidu, etc.

CIC Reports are now available on Bloomberg and FactSet portals.

About CIC

CIC is a professional consulting firm offering tailored end-to-end support across the full investment and financing lifecycle. The firm boasts a world-leading track record in guiding landmark first-in-sector IPOs across global markets, alongside unrivaled reach and in-depth coverage capabilities across specialized niche market segments.

CIC helps enterprises refine scalable business models and craft compelling capital narratives to enable seamless access to global capital markets, while serving as a trusted due diligence partner to investment institutions. It delivers granular industry insights and direct access to subject matter experts, empowering clients to identify high-value opportunities and mitigate critical risks effectively.

Media Contact